Consumer

When Does Back-to-School Shopping Start? (Hint: Earlier and Earlier)

Restaurant spending has remained remarkably steady in recent years despite inflation and soaring prices, but there are signs consumers are ever so slightly starting to finally pull back on dining out.

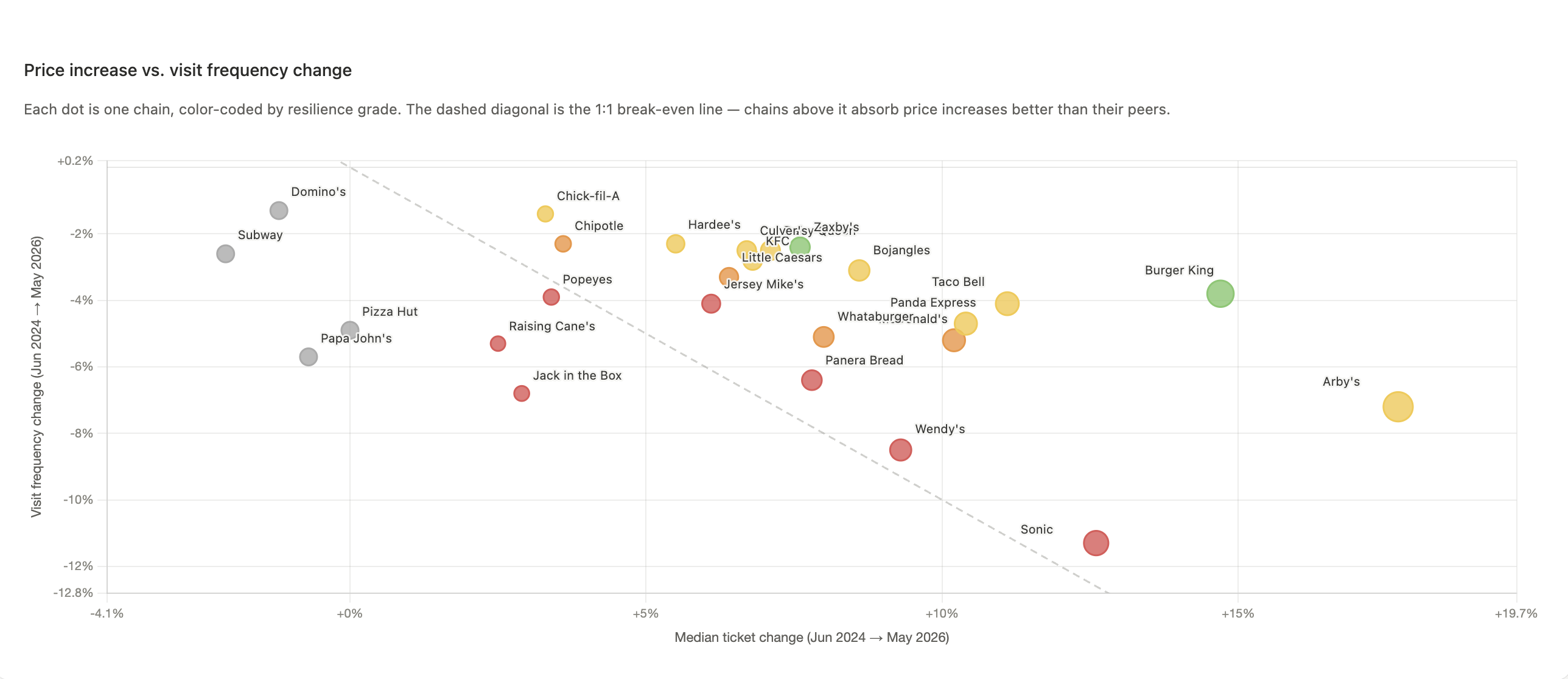

According to new data from Attain, Americans have trimmed how often they dine out by a few percentage points, yet they’re still pouring money into the industry by absorbing price increases many times larger.

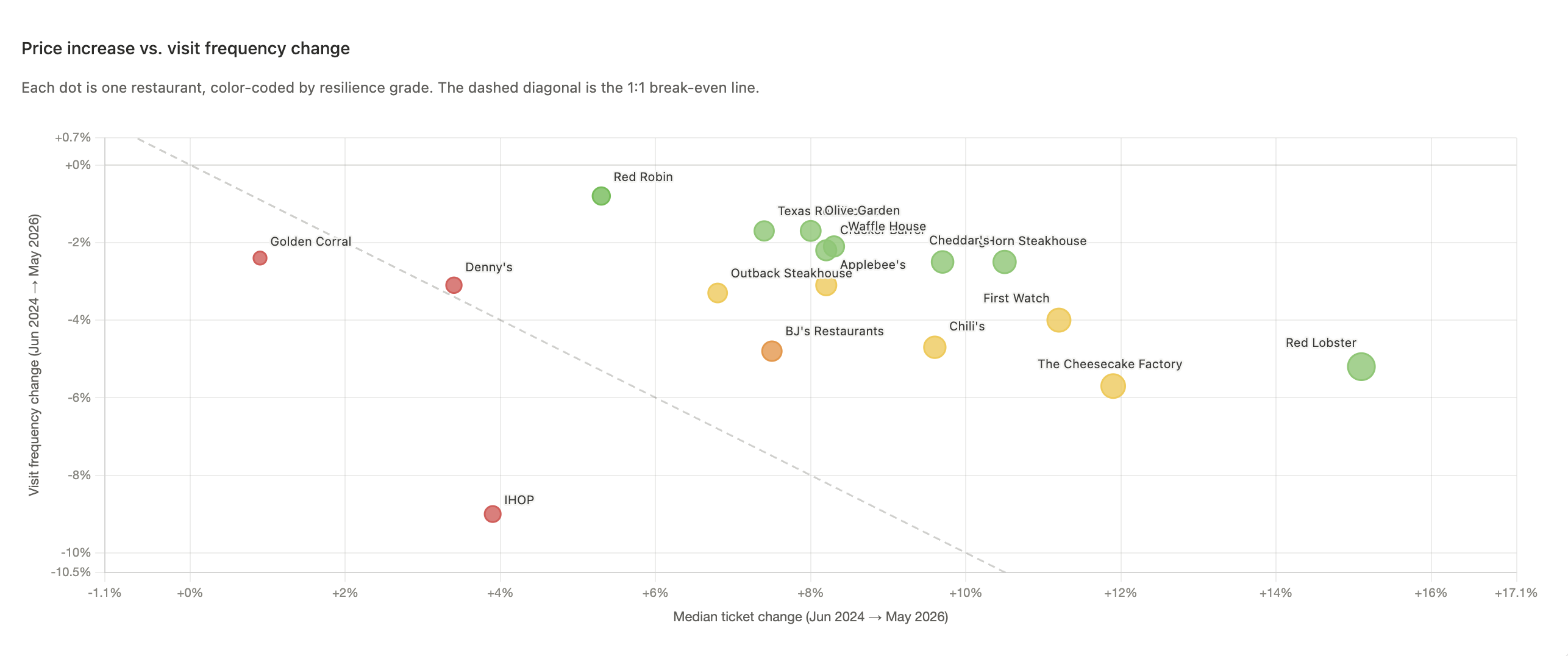

Fast-food prices rose about 6 percent on average over the past two years while visit frequency fell about 4 percent; sit-down prices rose 6 percent while frequency fell 3 percent. The price increases are substantial, but the consumer cutbacks are more modest. By that measure, dining-out demand in 2026 is still remarkably sticky for some, but not for all.

Dining out is one of the first categories consumers cut back on during times of economic stress. Anecdotally, consumers bemoan the $20 McDonald’s receipt and the $8 latte, and a recent (since deleted) Reddit thread went viral asking “What have you stopped buying now that the price is genuinely insulting?” The most cited category was fast food.

Prices for fast food have undoubtedly increased, anywhere from 2% (Raising Cane’s) to nearly 17% (Arby’s). Consumers are pulling back, but for a select few, loyalty and habit seem to outweigh price increases.

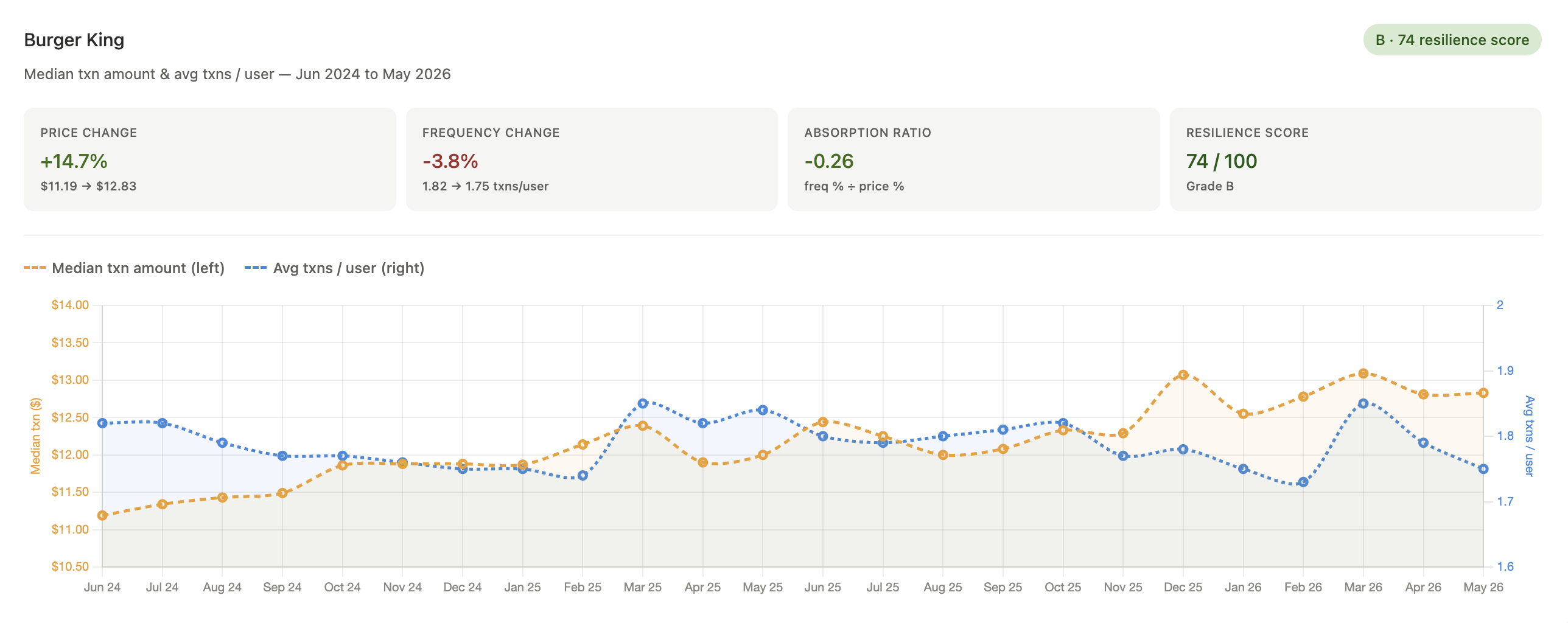

Burger King has the second highest ticket increase out of all QSRs analyzed at 15%, yet frequency has decreased by only 3.8%, making it incredibly resilient compared to other chains. Burger King has been steadily raising prices since 2024. According to some sources, this is to support higher worker wages and the increasing cost of beef, which is up 32% since 2023.

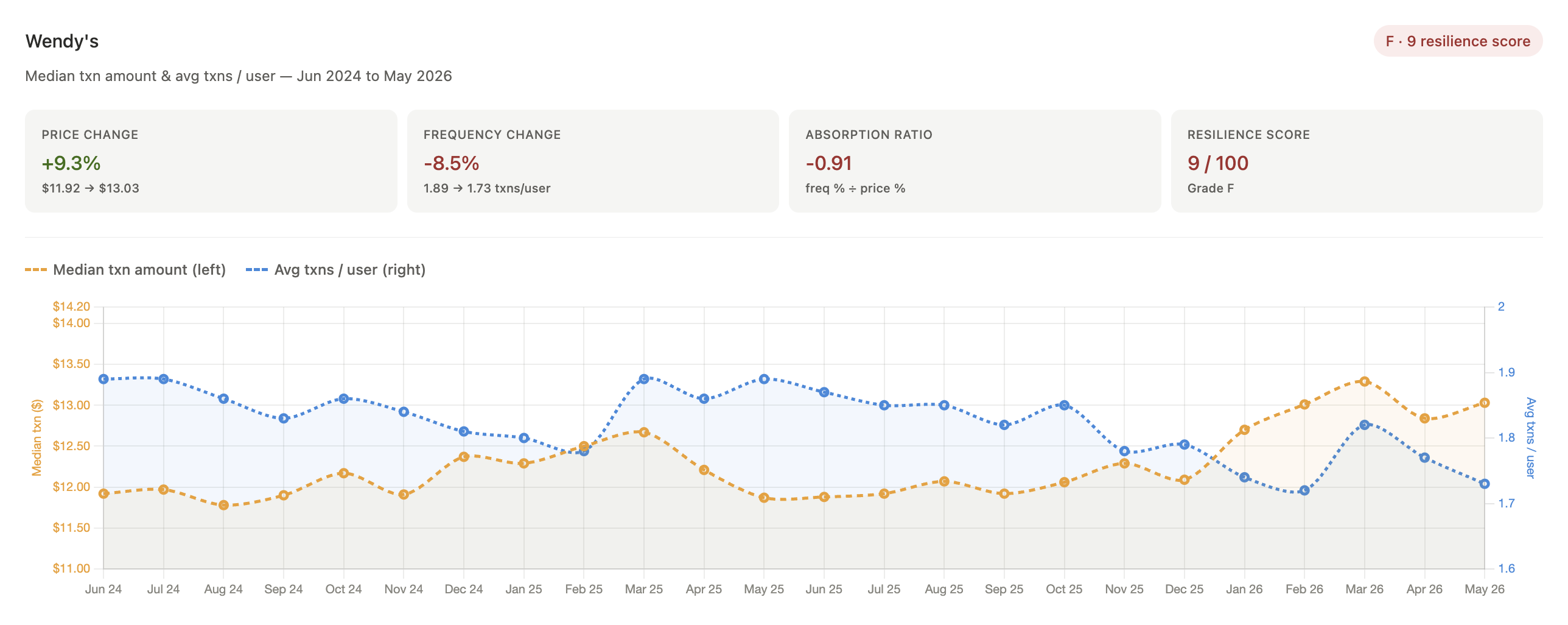

Despite more modest price increases, Wendy’s is not faring as well as Burger King. Frequency is falling in lockstep with rising prices, indicating that customers aren’t absorbing the price hikes willingly. The Attain data mirrors Wendy’s performance on a broader scale– its share price has fallen 48% in the last year and it’s closing hundreds of stores, according to The Financial Times. Why Burger King’s customers can withstand the significant increases while Wendy’s customers can’t is an example of a larger pattern found across the board, and one with more questions than answers. This could also be partially driven by geography and demographics. According to Attain data, Burger King skews older and higher-income than Wendy’s, and is geographically concentrated in the Midwest — particularly the East North Central division. Wendy's has a more balanced age and gender split, draws more evenly across income tiers and is stronger in the South and Sun Belt.

For many QSRs, median transaction amount started climbing in Q4 2025 and has continued to increase throughout 2026. Arby’s median ticket price has been rising steadily, from $13 in 2024, peaking at nearly $16 in December of 2025. This could be partially driven by the rising costs of beef and Arby’s’ beef-focused menu. They’re faring well considering, with visits per user only falling 7% compared to the 17% price increase.

There are four outliers — Domino’s, Papa John’s, Pizza Hut, and Subway — whose prices stayed flat or fell, but are still experiencing drops in visits. This indicates that chains maintaining pre-2024 prices are not being rewarded with increased patronage. However, three out of four are pizza restaurants, which already have a higher price per ticket than the typical QSR. Subway has been admirably steady in their prices, but is still seeing a bit of a drop in visits.

Overall, QSR is seemingly on a downward trajectory, with consumers being less and less willing to absorb costs when the product quality has remained constant, or in some cases, worse.

Unfortunately for QSR brands, there doesn’t seem to be a magic formula to guarantee loyalty while maintaining revenue. Panera, Sonic and Wendy’s are approaching break-even on revenue gained and lost in Attain data — meaning their increases in price are negated, revenue-wise, by corresponding decreases in customer purchase frequency.

Popeye’s, Jack-in-the-Box, and Raising Cane’s are potentially destroying customer demand by even meagerly raising prices. This might not be entirely their fault, but it seems that moderate or conservative price increases are not being recognized enough by consumers to move the needle in the brands’ direction.

Sit-down dining tells a different story from QSR, and is seemingly much more resilient to modest price increases. Intuitively, this makes sense, as consumers likely already expect to pay more when going out for a sit-down meal, especially to one of their favored dining brands. Sit-down dining might be less frequent than a stop at the drive-thru, so the check is probably subject to less scrutiny compared to a more frequent fast food transaction.

Attain data shows that while sit-down restaurant customers did index higher on household income than QSR, it wasn’t the sole cause of sit-down resilience. The restaurants with the highest income indexes (Cheesecake Factory, Panera, and BJ’s) all rated lower on resilience, while chains like Burger King — which tend to skew lower-income than the sit-down brands — show the opposite.

“A quick-service meal can feel expensive if it is purely transactional, while a full-service meal can still feel like a ‘value’ if it delivers hospitality, quality, consistency, and a memorable experience," Darren Spicer, a hospitality culture consultant, told The Outcome.

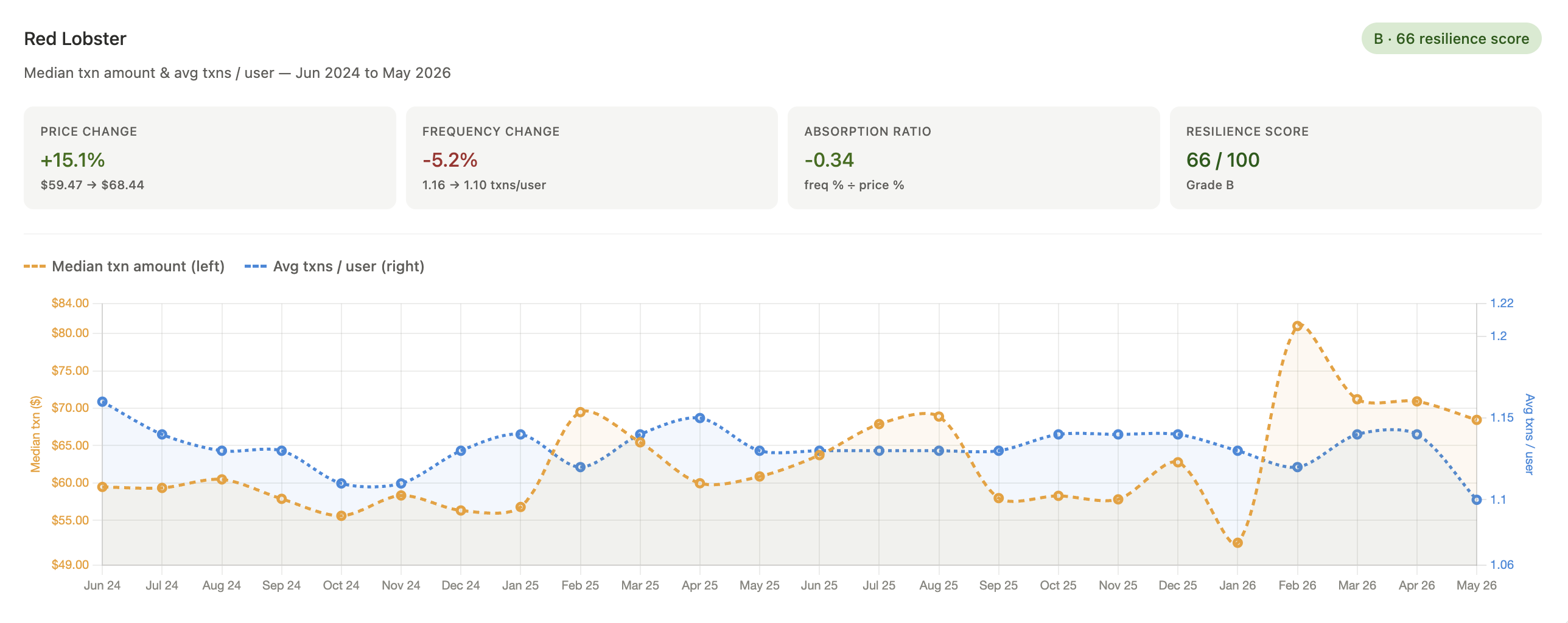

Even Red Lobster, the highest-priced chain in the analyzed data set, has increased transaction amounts by 15% over the last 24 months, while managing to maintain a steady visit frequency. The chain filed for bankruptcy in 2024 after making $20 “endless shrimp” a permanent menu item, which led to $11 million in losses. The data shows that despite its tumultuous couple of years, it still has a loyal fan base who make a visit to Red Lobster a monthly occurrence. That $11 million might have paid off by creating a sustainable and loyal customer base that remained even when the shrimp ran out.

This example suggests that resilience is a function of brand loyalty. Chains that raised prices most aggressively absorbed the increases best. This could reflect genuine customer loyalty, stronger brand equity, or simply that aggressive pricers were operating in less substitutable positions. In the case of Red Lobster, there aren’t many seafood restaurant alternatives that could take its place, especially in underserved areas.

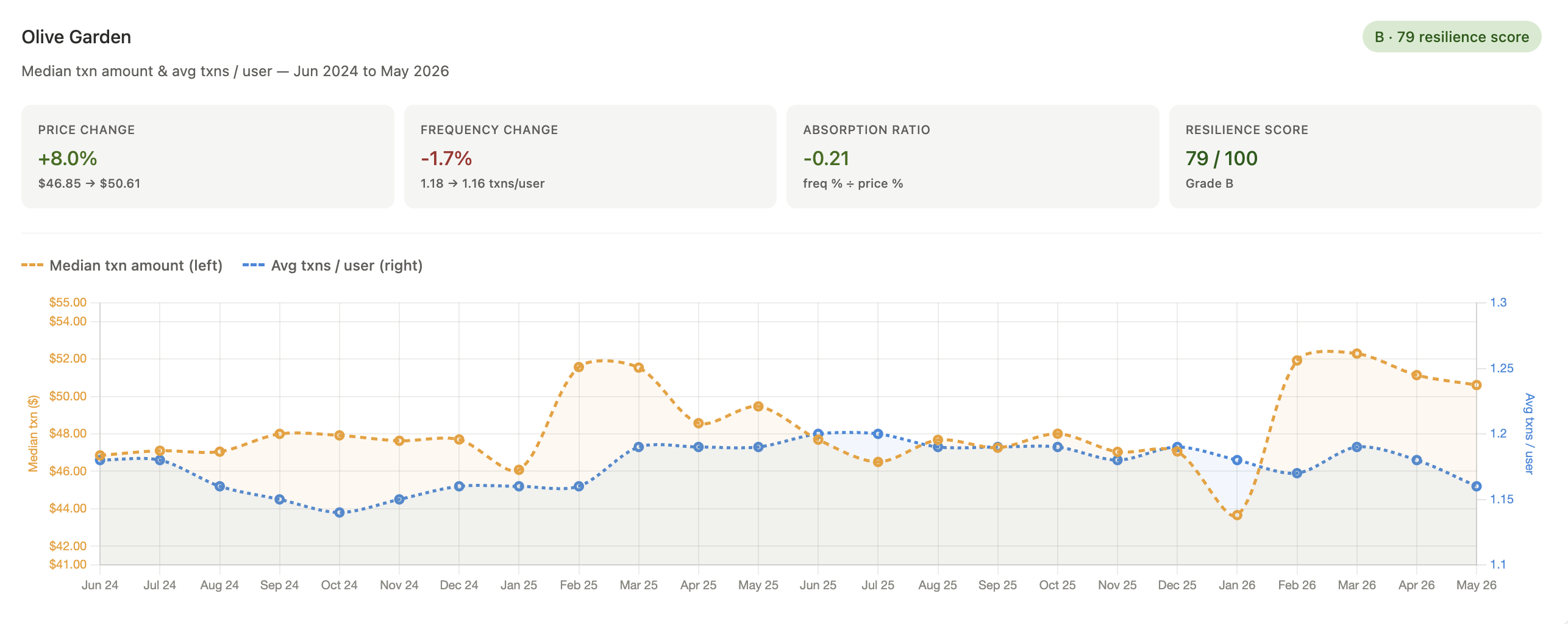

Generally speaking, 2026 seemed to be a turning point across the board for price hikes. For the first 4 months of the year that this data covers, many consumers haven’t noticed or cared that their bill has increased a couple of dollars. A dollar here or there on a menu item from Olive Garden (perhaps paired with a glass of house Chianti) will hurt less than a dollar more on an already lackluster hamburger from a QSR chain during a 30-minute lunch break. The Olive Garden data shown below shows a $5 ticket increase from 2025 to 2026, yet consumers have barely blinked an eye. For sit-down, consumer state-of-mind seems to be the behavioral driver that wins out.

Sarah White, the owner of the full-service restaurant Westover Taco in Arlington Virginia, said she’s had to raise prices 8% in recent months, yet customers barely batted an eye.

“What will they remember when they leave? If it is the service, food, and atmosphere then you will survive the price increases,” White told The Outcome. “If it is the price, then it isn't the price you need to be worried about. Focus on better service, quality, and experience until the price makes sense.”

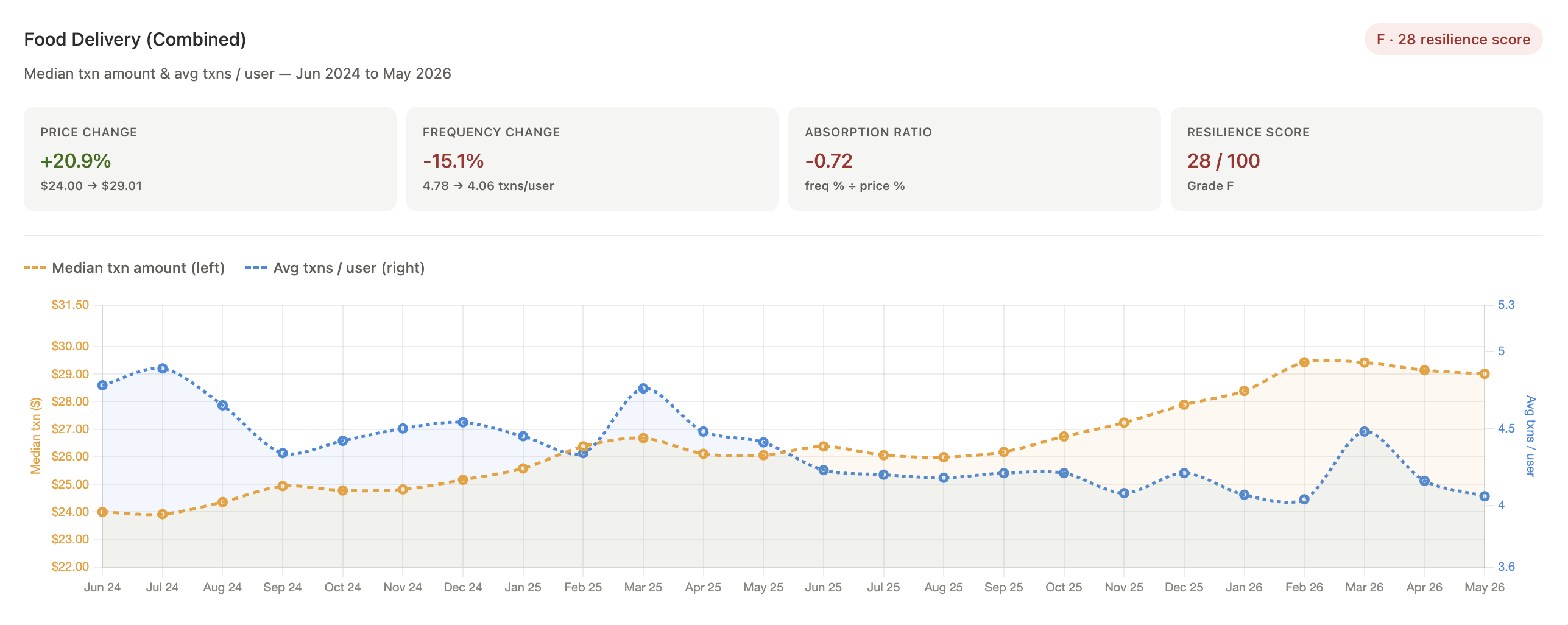

In 2024, three out of four restaurant orders were not eaten in the restaurant, according to data from the National Restaurant Association. Delivery apps are ubiquitous, but according to Attain data, they have had the most dramatic jump in costs over the last 24 months out of all three categories. Transaction amounts across all three major apps (DoorDash, UberEats, and GrubHub) have risen 20% since 2024. DoorDash started with the lowest average transaction amount out of the three at $23.83, but has since risen to over $31, a nearly 30% increase. Though average frequency per user is falling, delivery apps are still considered resilient because earned revenue outweighs customer churn.

Overall, food delivery app users were transacting nearly five times a month in June of 2024, or more than an order a week. As of spring of 2026, the monthly average has dropped to around four. Consumers scaling back by about one order a week, but by no means an exit from the category.

Unsurprisingly, Attain delivery app users are younger (25–44), more diverse, slightly higher-income, and overwhelmingly concentrated in coastal and Northeastern metros. They seem to have a high tolerance for paying for convenience, even if it adds on 20-30% to the bill.

Dining out today is a sticky consumer behavior yet also nuanced. Customers aren’t willing to blindly fork over their dwindling disposable income for a subpar meal. They want experience, value, quality and convenience, and usually some combination of all four. As one Reddit user put it, “it shouldn’t cost $27 to feed two people food that comes in a box handed through a window.”

Thanks for reading our first article in The Outcome’s new series The Breaking Point. View the data from this article in our interactive dashboard. Stay tuned for more coming soon!