Consumer

Consumers Say They’re Pulling Back, But Purchase Data Shows Otherwise

Consumers' relationship with alcohol is undergoing a major upheaval, with younger generations loosening the grip booze has had on the human race for the last 10,000 years. Every January, headlines flood in about a mass retreat from drinking — Dry January has become a cultural touchstone, a badge of wellness worn proudly into the new year. But what does the actual purchase data say? Quite a different story.

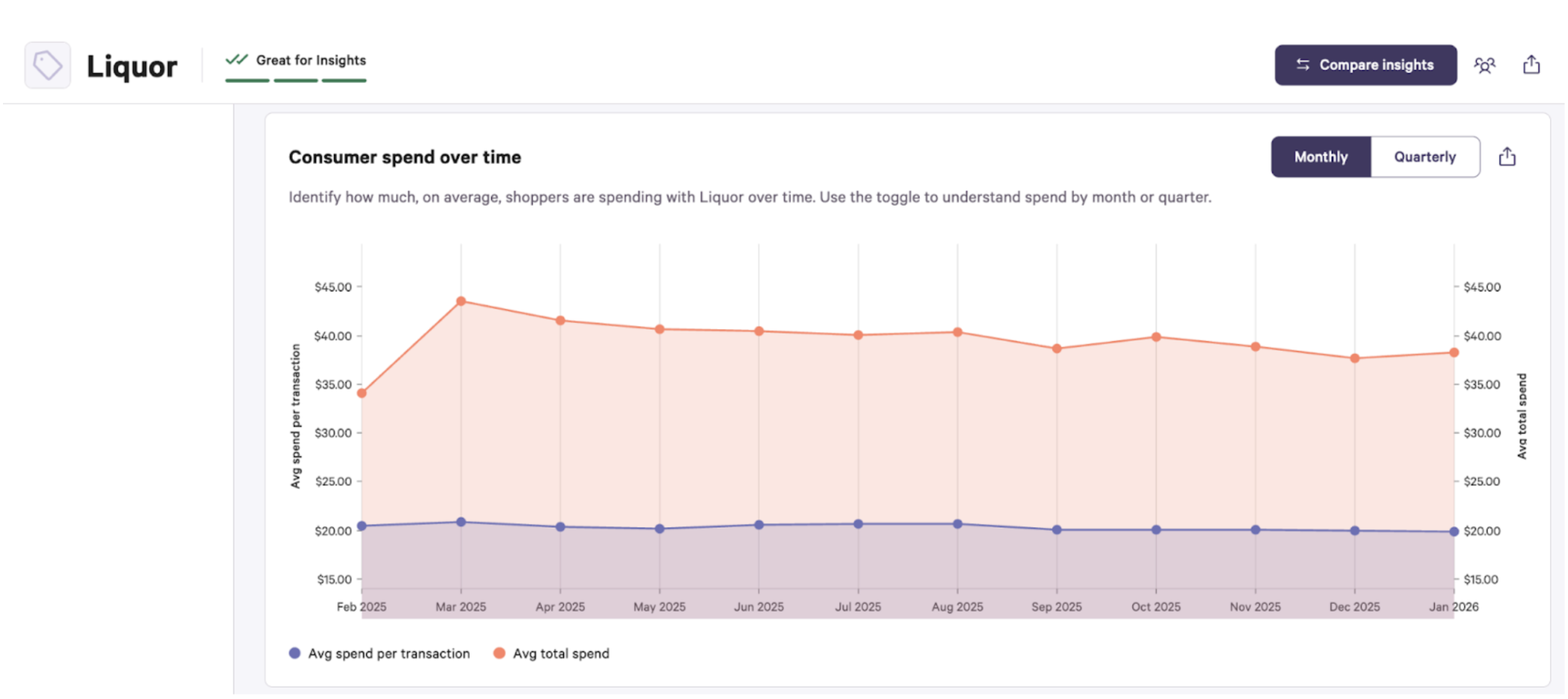

If Dry January is a movement, it's one that hasn't made it to the checkout counter. Attain's consumer spend data for liquor shows that average spend per month held remarkably steady throughout 2025 and into January 2026, hovering around $30 with no meaningful dip in the new year.

This isn't entirely surprising. Dry January, for all its cultural cachet, has always been more of a social media phenomenon than a mass behavioral shift. The people talking about it loudly online may not represent the broader buying public. For alcohol brands and retailers, the data is actually reassuring: January is not the threat it's been made out to be. The real disruption is playing out on a much longer timeline — and it's generational.

Look at the demographic breakdown of who's actually buying alcohol, and one generation stands out: Gen X (born 1965–1980). In the liquor category, Gen X makes up 35.3% of buyers and carries a High index score of 128, meaning they over-index significantly compared to their share of the general population. Millennials (27.9%) and Boomers+ (23.6%) come in as neutral, while Gen Z (13.4%) is notably Low, with an index score of just 71.

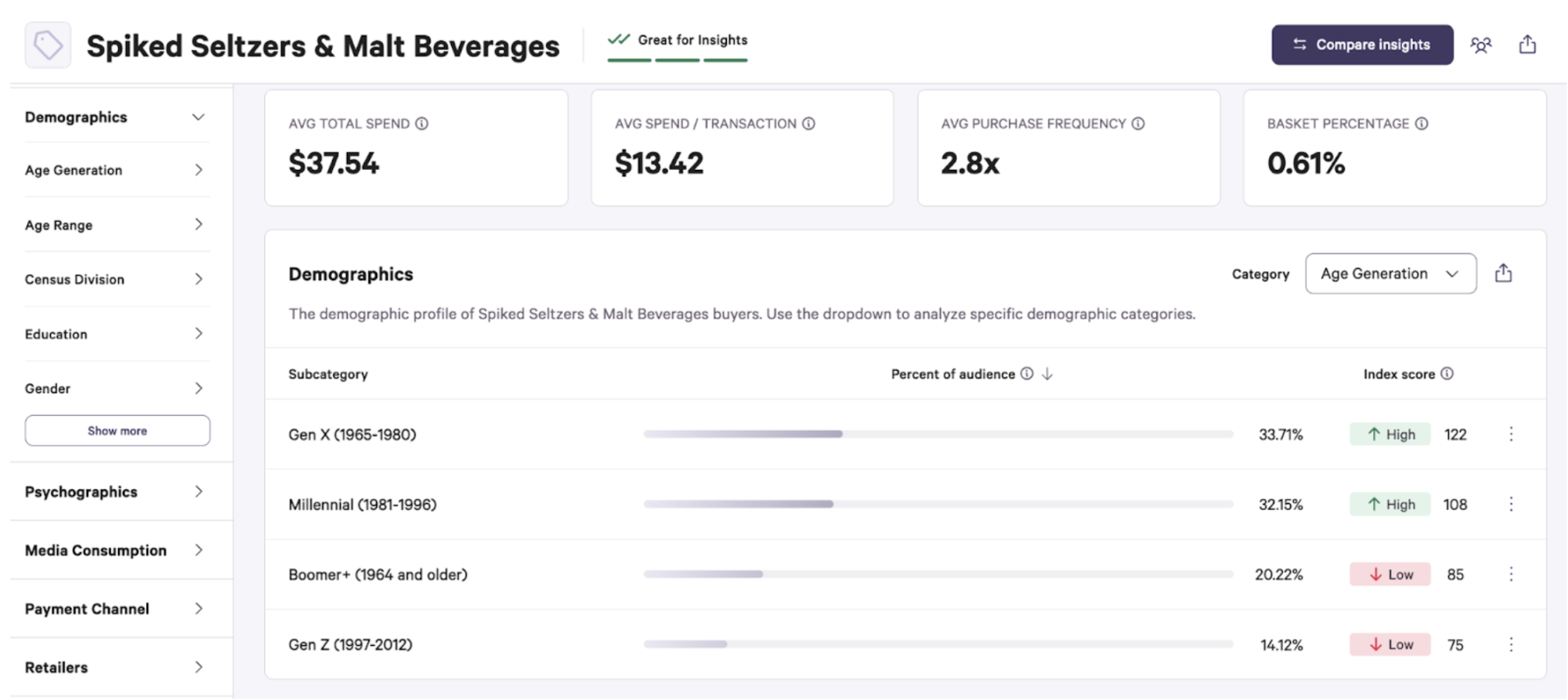

The story is even more striking in Spiked Seltzers & Malt Beverages — a category that was essentially invented for younger drinkers. Despite the White Claw-and-Truly marketing aesthetic, Gen X leads here too, at 33.7% of buyers with a High index of 122. Millennials are close behind at 32.2% (also High), while Boomers+ and Gen Z both skew Low. The generation that came of age with grunge and flannel has apparently also claimed hard seltzer as their own.

The scale of Gen Z's disengagement becomes even clearer when you look at total annual spend. According to U.S. Bureau of Labor Statistics data, Boomers, Gen X, and Millennials each spend north of $23 billion annually on alcoholic beverages. Gen Z spent $3.13 billion — a fraction of every other generation, and a gap that can't be explained by age alone.

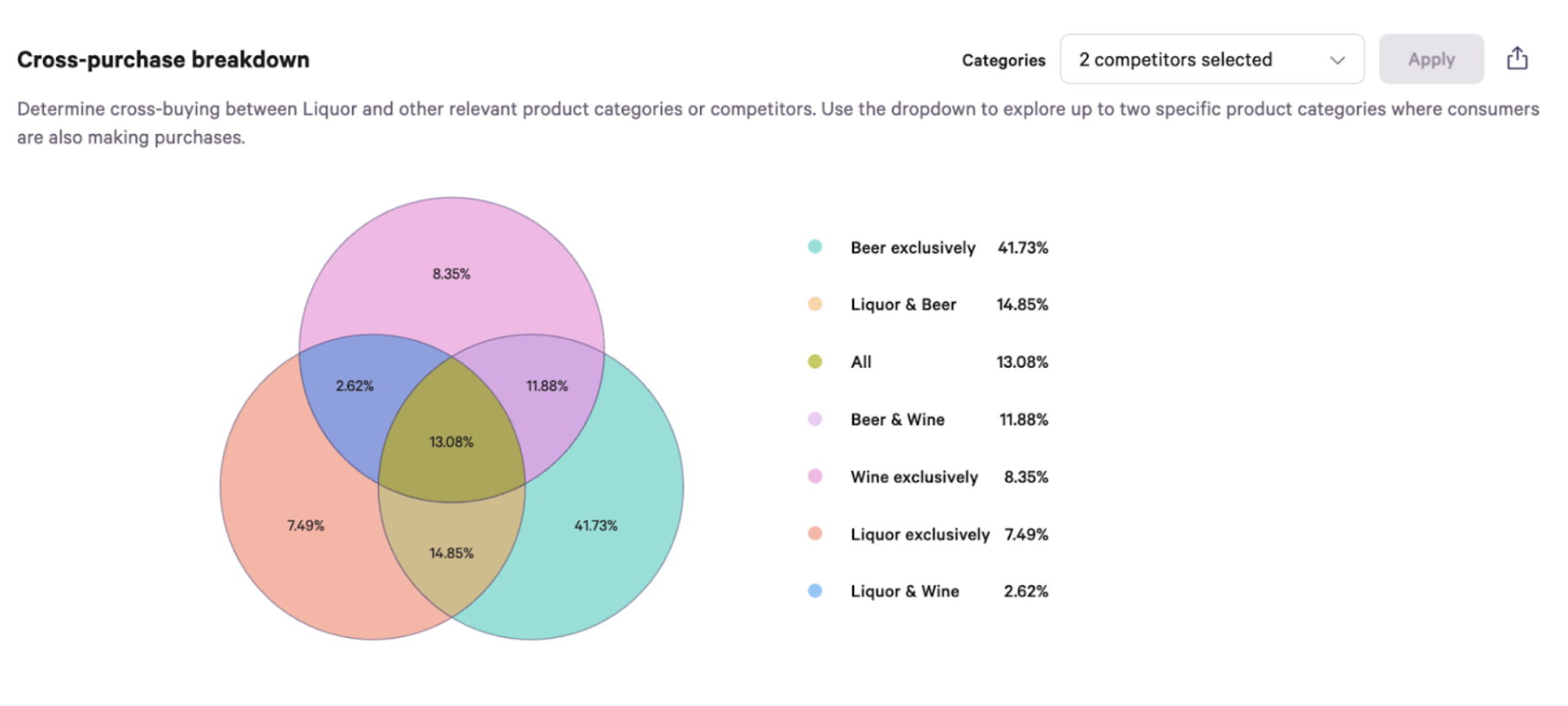

The cross-purchase breakdown reveals just how siloed beer drinkers tend to be. Of the consumers analyzed, 41.73% buy beer exclusively, by far the largest single segment. Only 14.85% buy both liquor and beer, and just 13.08% buy across all three major categories (beer, wine, and liquor). Wine-exclusive buyers account for 8.35%, and liquor-exclusive for 7.49%.

This has meaningful implications for the industry. Beer's massive consumer base is largely self-contained, showing that beer drinkers will not typically drift toward a premium spirit or a glass of wine. Cross-category upsell is a harder play than it might appear. For beer brands, loyalty runs deep, but it also runs narrow.

Here's where the picture gets genuinely sobering: even among beer buyers, typically seen as a lower ABV, every-day drinking option, most consumers are anything but loyal drinkers. Ultralight Buyers make up the largest segment at 36.63%, purchasing at a frequency of just 1.0x per period and spending an average of only $13.26. Light Buyers add another 24.28% at 3.3x frequency and $45.47 in spend. Together, that's over 60% of beer buyers who are low-frequency, low-spend consumers.

Heavy Buyers — those purchasing 20.3x per period and spending an average of $336.32 — represent only 20.57% of the audience. Sometimes Buyers (18.52%) sit in the middle at 6.8x frequency and $103.26 in average spend.

The alcohol industry's revenue engine is running on a relatively small group of older, heavy buyers. And the culture data is clear: younger generations are drinking less, experimenting with non-alcoholic alternatives, and showing up in purchase data at a fraction of the rate of their predecessors. The best customers the industry has may also be the last of their kind.

The data offers some useful signposts for where to focus energy and budget.

Don’t sleep on Gen X. They're over-indexing across every category, including ones largely marketed to younger consumers. There's a strong case for campaigns that speak to them more directly rather than treating them as a secondary audience.

Rethink the Gen Z approach. An index score of 71 in liquor suggests this cohort's relationship with alcohol is genuinely different — not just delayed. Reaching them may require a different product strategy (lower-ABV, non-alc adjacency) rather than just different creative.

See light and ultralight beer buyers as an opportunity. They make up over 60% of the beer audience. Even small gains in purchase frequency among this group could move the needle meaningfully — occasion-based marketing and loyalty programs are natural places to start.

Treat beer drinkers as their own audience. With 41.7% buying beer exclusively, cross-category strategies are a harder sell than they might seem. These consumers are loyal to the category, and messaging that meets them there will likely outperform broader portfolio plays.

Start cultivating the next heavy-buyer cohort now. The current base of high-frequency, high-spend buyers is older. Gradually moving Sometimes Buyers up the loyalty curve is a longer-term play worth starting sooner rather than later.

The Bev-Alc industry has weathered plenty of shifts — the craft beer explosion, the wine boom, the hard seltzer moment. A generational change in consumption behavior is a slower, subtler challenge, but the brands paying attention to the data today will be better positioned for what comes next.

Data and insights sourced from Attain's platform OutcomeHQ.